The Indian government has rightly made rooftop solar power one of its top clean energy priorities – here’s how they can jumpstart the nascent market.

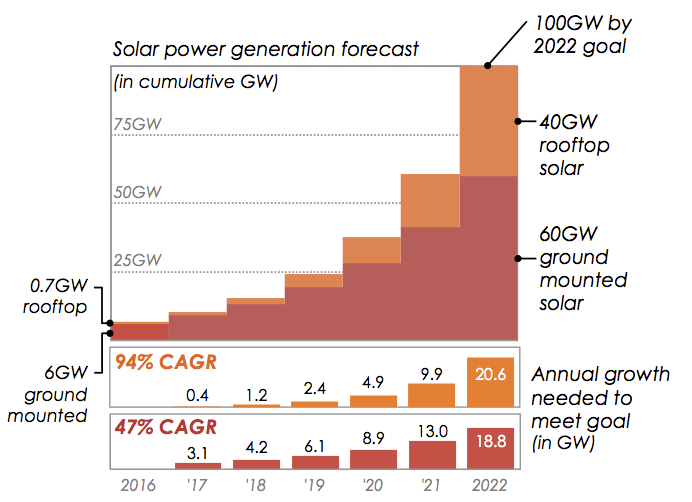

With a bold goal of delivering 100 GW of solar power by 2022 India is helping to create one of the world’s fastest growing solar markets. Impressive strides have been made towards building out the 60 GW of utility-scale solar power necessary to make good on the goal. However, the remaining 40 GW of rooftop solar power needs a boost. Getting this market right can help put a serious dent in the energy poverty suffered by 80 million households currently lacking electricity, and is critical for supporting the country’s growing middle class.

Rooftop solar power has enormous potential in India and has experienced steady growth in recent years. It offers electricity consumers a lower electricity bill (on average 30% savings for businesses and 18% for industry), and a reliable alternative to intermittent electricity from the grid. The problem is, while the market is growing at a “blistering 300% pace”, even more is needed to get from approximately 1 GW today to 40 GW in 2022. A new report from Climate Policy Initiative (CPI) shows a few ways we can unleash even greater growth.

Support Third Party Financing

A third party financing model consists of a rooftop solar developer, a third party financier, and a consumer. The developer installs a rooftop solar plant on a consumer’s property and the third party financier invests in the project. The consumer agrees to purchase electricity at a specified price for 15 to 25 years, with no upfront cost except their monthly electricity bill. The third party financing model removes the burden of high upfront installation costs for the consumer, as well as perceived performance risk, or the perception that the technology may not perform as expected over its lifetime.

The third party financing model has been a significant driver of growth in the rooftop solar industry globally, especially in the US where up to 72% of rooftop solar installations in 2014 were third party-owned. The model has also started picking up recently in other countries, including China and Japan.

But in India it only supports 13% of rooftop solar installations under operation or construction. The industry believes that there is potential to increase the total installed capacity under the third party financing model to more than 20 GW by 2022, meaning that it could unlock more than half of the government’s 40 GW target.

The third party financing model is also a good opportunity for investors. With government incentives, all states in India offer internal rates of return (IRR) of at least 14% and as high as 42% for rooftop solar projects financed by third parties. And, as the cost of solar falls, more sectors in Indian states are becoming profitable without these incentives. Over 40% of the opportunities already offer IRRs of 14%-34% even without government incentives.

Train Banks to Help Unlock Local Debt

It’s no secret the solar business is capital intensive. That means access to debt finance is critical to its long term success. Since the rooftop solar sector is new and transaction costs are high (due to the smaller size of projects), bankers don’t yet feel comfortable lending to projects. The most significant challenge to the third party financing model today is low access to debt finance.

To increase access to debt for rooftop solar power, the Ministry of New and Renewable Energy (MNRE) can work with development banks to provide a system of trainings to bankers in India to increase their understanding and comfort with rooftop solar loans. Trainings can include how to assess rooftop solar projects, how to process solar loans, and the dynamics of the rooftop solar industry and associated risks.

Given the depth and breadth of the local banking system, and the $625 million it now has to solve this problem thanks to the World Bank, high leverage interventions like these can get the money flowing.

Get DISCOMs in the Game

Another important step is addressing consumer credit risk. Consumer credit risk is the second biggest challenge to the third party financing model. Low availability of credit assessment procedures, low enforceability of agreements, and lengthy and costly legal processes in the case of a dispute or payment default all conspire to hold back investment.

One way to reduce consumer credit risk is for MNRE and state governments to include India’s state-level public electricity distribution companies (DISCOMs) as a party to the power purchase agreement between the developer and the consumer. While DISCOM balance sheets don’t exactly inspire confidence, they do have the power to terminate grid supply which can provide an effective ‘stick’ to ensure customer payment.

DISCOMs are also responsible for implementing net metering, which is a policy that has been passed in nearly all states that makes rooftop solar power more viable by enabling consumers to use solar power generated during the day at night. However, at present, there is little incentive for DISCOMs to prioritize net metering implementation which means most rooftop solar companies don’t take advantage of it. One way to overcome DISCOMs’ reluctance would be to incentivize them to fulfill their Renewable Purchase Obligation (RPO) requirement – a government requirement to install solar power – via rooftop solar installations, by providing 30% more credit to rooftop solar power generation compared to utility-scale solar power.

Invest in Financial Innovation

Last but not least it’s clear that financial innovation has been key to unlocking clean energy abroad, and it is likely to be useful inside India as well. The India Innovation Lab for Green Finance, a public-private initiative, administered by CPI and modeled after the successful Global Innovation Lab for Climate Finance, is currently developing several instruments which have the potential to drive significant investment into third party financing for rooftop solar power.

The first, Loans4SME, is a peer-to-peer lending platform that connects investors directly with borrowers and could help improve access to debt financing for the rooftop solar industry. The second, the Rooftop Solar Sector Private Financing Facility backed by the IFC, could increase access to debt financing for the rooftop solar industry by creating a warehouse structure that aggregates and purchases large numbers of small projects helping to inject liquidity into the market. This also enables an aggregate deal size large enough and of sufficient credit quality to attract more attention from investors, especially institutional investors.

Taken together, these policy and financial solutions can jumpstart India’s rooftop solar industry and put it on track to achieve the government’s target of 40 GW of rooftop solar power by 2022, a goal the whole world should get behind.

This post was co-authored by Gireesh Shrimali of CPI and Justin Guay of the David and Lucile Packard Foundation. A version of it first appeared in Greentech Media and also in The Huffington Post.