Mobilizing investments by institutional investors, foreign and domestic, is a requisite for India to meet its clean energy targets. India needs an additional ~450 billion of capital by 2040 to reach ~480GW of renewable energy capacity. Foreign institutional investors with USD 70 trillion and domestic institutional investors with USD 560 billion of assets under management may prove crucial in fulfilling the financing requirements of this sector.

In this paper, we develop a business case for institutional investors to invest into the renewable energy sector in India. We start by identifying key drivers for renewable energy investments in India. We then explore the alignment of the investment criteria of institutional investors with renewable energy. Finally, we discuss barriers to renewable energy investments as well as strategies to overcome them. To this end, we interviewed more than 50 foreign and domestic stakeholders, including: pension funds, sovereign wealth funds, family funds, investment advisors, developers, associations, regulatory authorities, brokerage houses, asset managers, and investment bankers.

We find that while the renewable energy sector in India offers an attractive investment opportunity that is well matched with the needs of institutional investors, there are still barriers to investment.

Our analysis shows that Indian renewable energy has moved from an early stage investment opportunity, characterized by high risk and high growth, towards one with low-medium risk and medium-to-high growth. At present, renewable energy investments are very similar to yield generating investments, with high growth potential.

India as a market is strong and economically attractive compared to other similar markets across the world. It benefits from strong policy commitments as well as a large market size (~480 GW capacity addition over 2016-40) that is third only to China and the United States. India is ranked 2nd in Ernst & Young’s renewable energy country attractiveness index. On a risk adjusted basis, India also offers higher excess returns1 of 3.5% compared with the US (2.4%) and China (1%).

In India, the renewable energy sub-sector is more attractive than other infrastructure sub-sectors, in particular fossil fuel power generation. Our analysis shows that coal plants exhibit greater cash flow variability (i.e. 40%) as compared to wind (i.e., 20%) and solar (i.e.,10%). Further, fossil fuel based power companies are currently witnessing a trend of a shrinking gap between their return on capital employed and the cost of capital, which has eroded their attractiveness.

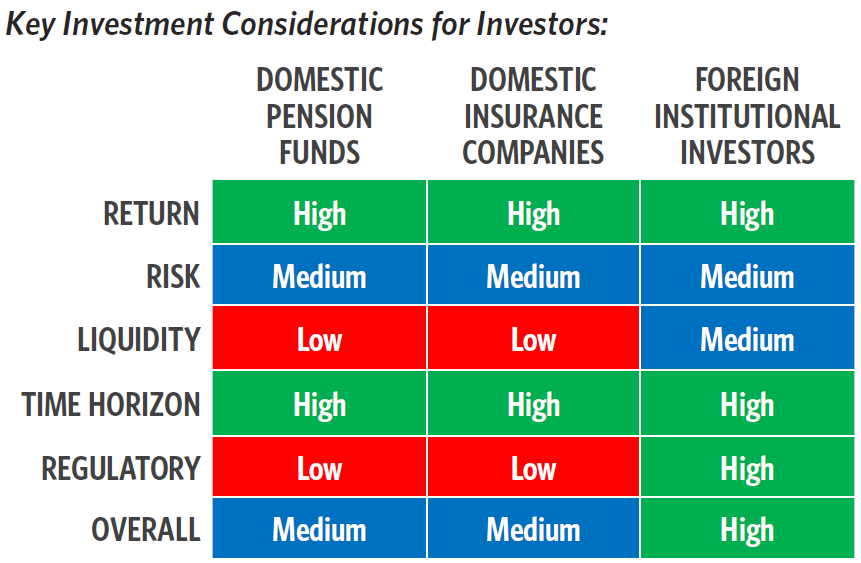

Renewable energy investment traits align reasonably well on key criteria such as return, risk, and time horizons, but illiquidity and regulatory restrictions remain.

A summary of the renewable investment profile against the investment considerations for institutional investors is shown below.

Domestic Institutional investors with long-term investment horizons are mostly seeking yield generating investments in low risk and long duration assets, i.e., traits that align well with the investment profile of renewable energy. With appropriate credit enhancement and regulatory and policy changes, the sector can provide a high match with domestic institutional investors’ investment objectives.

For foreign institutional investors, the renewable energy investment landscape has changed from small size and high risk-high return investments to large size and medium risk- moderate return investments. Although the expected return from renewable energy projects has come down from 20% to 15%, this still matches their overall India market portfolio return requirements. Higher returns are still possible through equity investments at the corporate level.

However, despite this apparent match, there are still barriers for institutional investment in renewable energy.

The key challenges, ranked by severity of the risk, faced by both domestic and foreign institutional investors include:

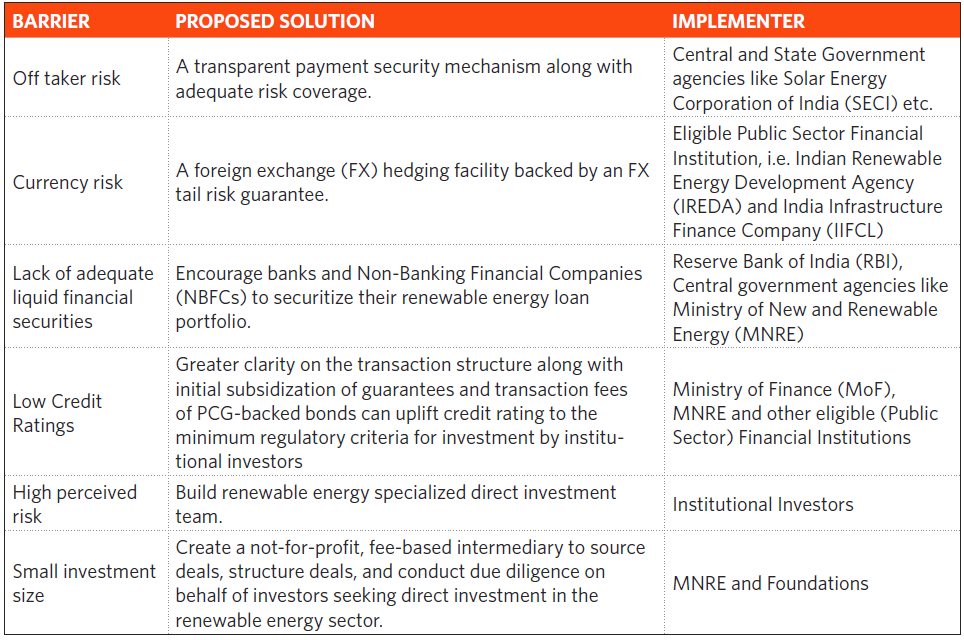

- Off-taker risk due to unwillingness and inability to pay, or refusal to off-take power, by the primary off-takers, the DISCOMS;

- Currency risk resulting from the need to finance renewable energy projects in India with foreign capital (e.g. USD), which exposes the borrower/ investor to the risk of currency devaluation of INR as the cash flow of the project is INR;

- Lack of adequate liquid vehicles related to the inability to sell investments at a fair price at any time;

- Low credit ratings, related to renewable energy debt vehicles not meeting minimum regulatory criteria on ratings;

- High perceived risk, related to the lack of historical performance data about the renewable energy sector;

- Small investment size, related to not meeting investors’ minimum investment size criteria, leading to high transaction cost;

In order to scale institutional investment in renewable energy to its potential, policymakers and regulators will need to address some of these barriers. Institutional investors, themselves, can also work toward investment practices that overcome other barriers.

To address the aforementioned barriers, based on a preliminary assessment, we suggest potential solutions for various stakeholders, as below.