Waste not: Time to rapidly scale methane abatement finance in the waste sector

The waste sector is responsible for approximately 20% of methane emissions, the second largest greenhouse gas after carbon dioxide. Without urgent action and adequate climate finance, waste sector’s methane emissions are projected to double by 2050, jeopardising the ability to stay within a 1.5°C warming scenario.

Methane emissions have contributed to about a third of global net warming since the Industrial Revolution. This short-lived climate pollutant has an average lifetime of a decade and 86 times the warming potential of CO₂ over 20 years. Anthropogenic (human-caused) methane emissions can be reduced by up to 45% this decade through low or negative costs solutions and readily-available technologies, avoiding nearly 0.3°C of global warming by 2045. According to the Global Methane Assessment, tackling this super-pollutant could also prevent over 255,000 premature deaths, 775,000 asthma-related hospitalizations, and 73 billion hours of lost labour due to extreme heat annually. Therefore, abating methane emissions is often considered the most effective strategy to stay within a 1.5°C warming scenario.

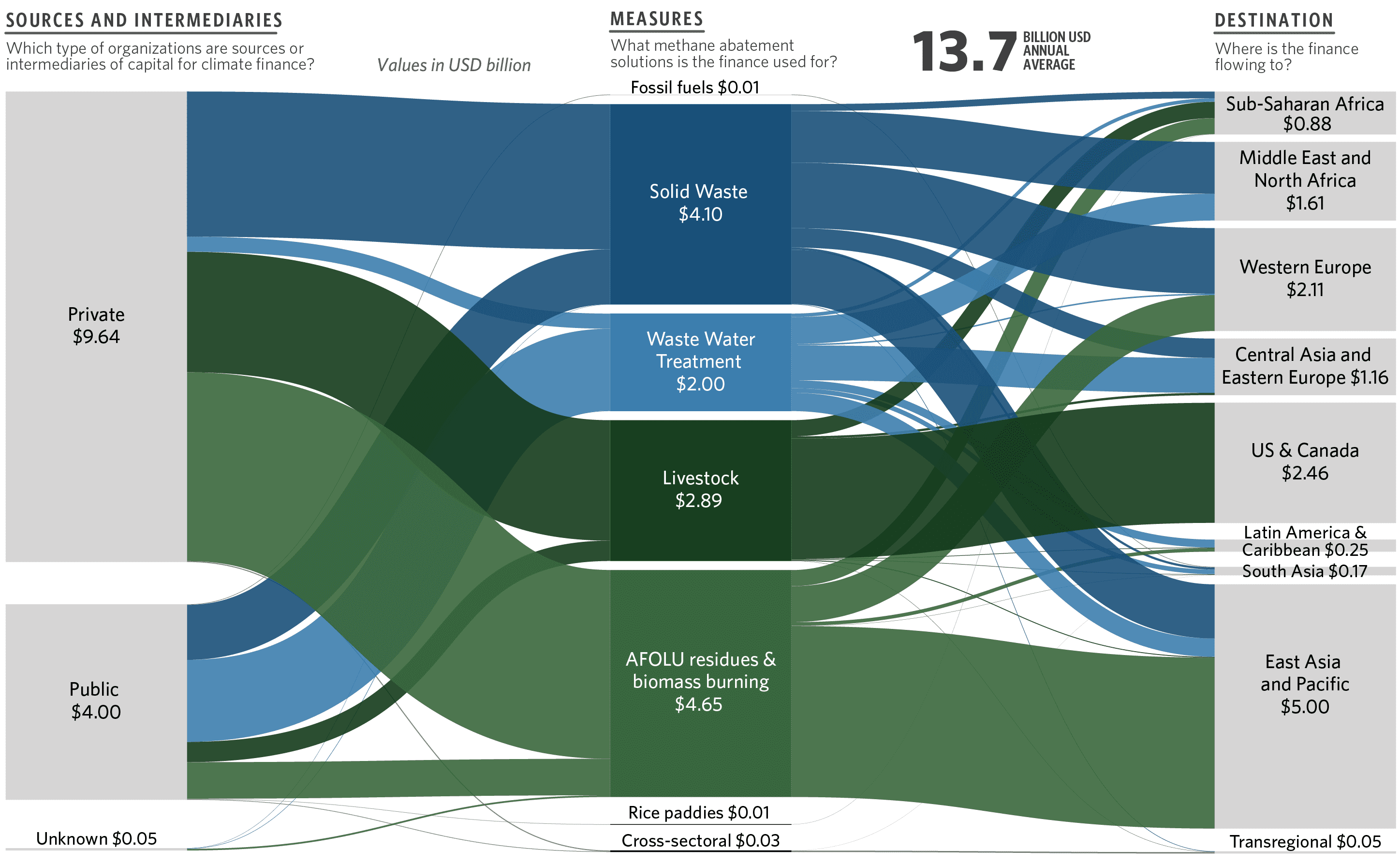

Despite methane’s significant contribution to climate change, CPI’s Landscape of Methane Abatement Finance 2023 shows that financial flows to abate methane account for only 1% of tracked global climate finance (USD 13.7 billion out of USD 1.3 trillion for 2021/2022).

Figure 1: Landscape of Methane Abatement Finance in 2021/2022

The waste sector is one of the most rapidly growing sources of anthropogenic methane emissions, contributing 20% of the total, as the third-largest source after fossil fuels and agriculture, forestry, and other land use (AFOLU).

In the solid waste subsector, methane emissions arise from the decomposition of organic waste in anaerobic environments such as landfills and waste dumps. Despite its significant contribution to climate change, action to abate methane in the waste sector remains critically underfunded.

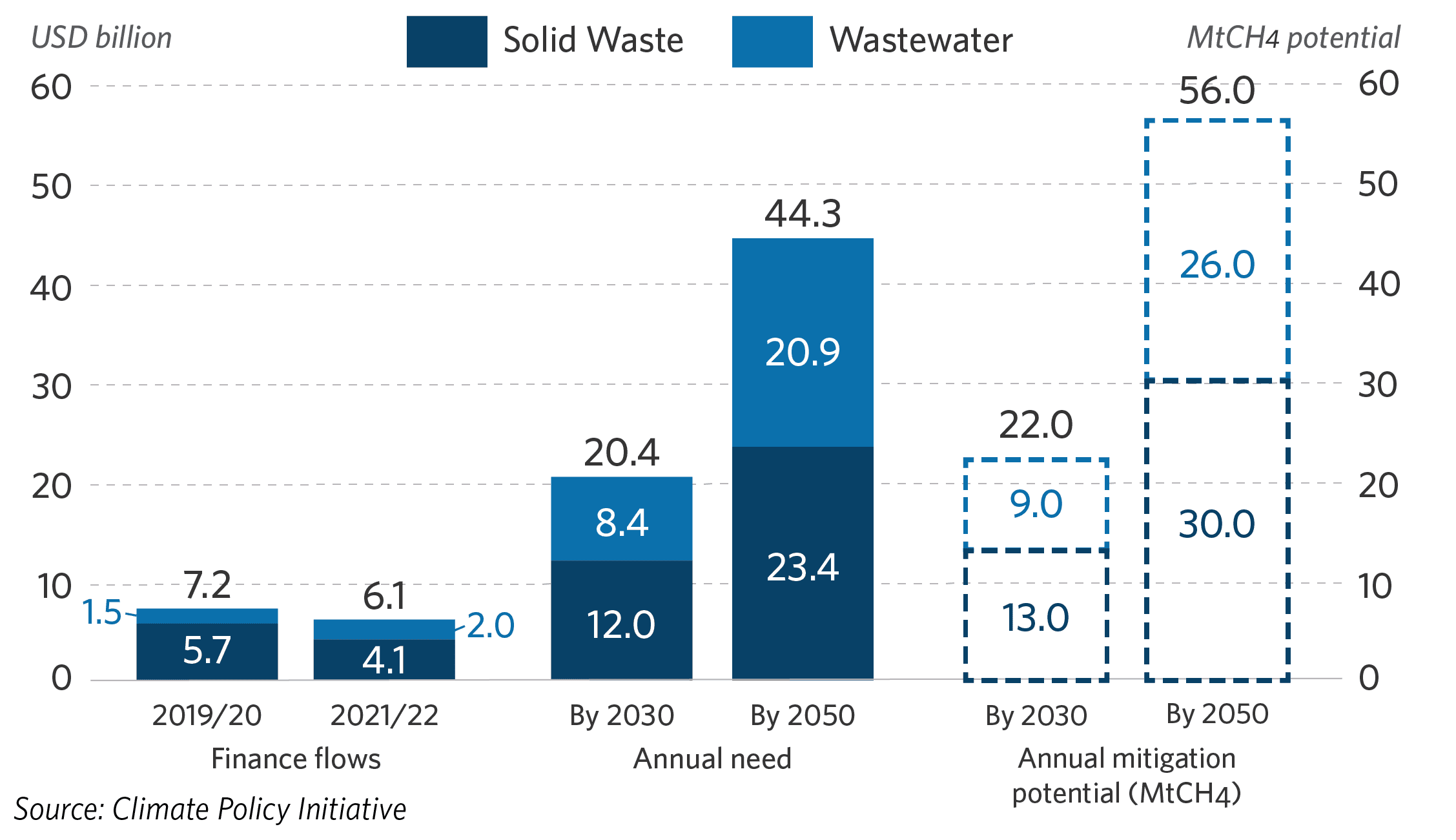

Figure 2: Methane abatement finance to the waste sector compared to needs and annual mitigation potential

Just USD 4 billion went to solid waste methane abatement in 2022, far below the estimated USD 12 billion required annually to achieve the subsector’s needs (see Figure 2).

Yet, UNEP’s Global Waste Management Outlook highlights that, under a business-as-usual scenario, the full net cost[1] of waste management (including hidden costs such as pollution, poor health, and climate change impacts) is projected to nearly double by 2050—from USD 361 billion (2020 baseline) to USD 640.3 billion (see Figure 24 in UNEP’s 2024 report). Conversely, getting “waste under control” by 2050 could avoid over USD 370 billion in full-net costs, while a circular economy scenario could achieve net gains (where recycling revenues outweigh environmental and health externalities) of more than USD 100 billion. Therefore, tackling waste management and the subsector’s methane emissions early on can prove to save hundreds of millions of dollars to all pillars of government in the future.

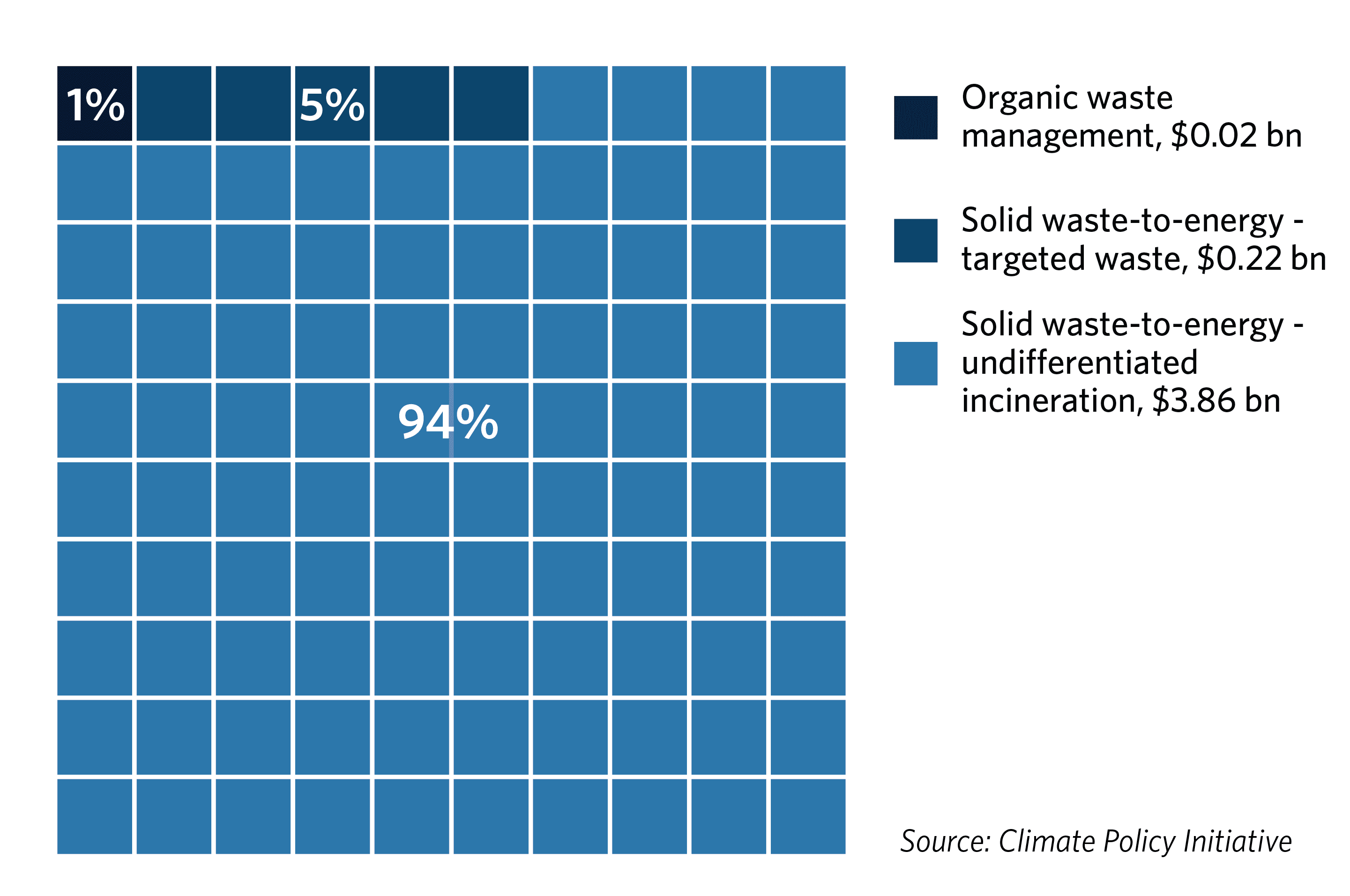

Currently, only 6% of the tracked solid waste subsector funding was directed toward best-available climate strategies, such as landfill gas capture and food waste anaerobic digestion (see Figure 3). Organic waste management, a critical methane abatement strategy including composting projects, received a mere USD 22 million of tracked global climate finance in 2022.

Figure 3: Methane abatement finance flows by strategy in the solid waste subsector in 2021/2022

The remaining 94% went to waste incineration, which generates energy, but also converts methane into CO₂, a method that is considered by some to be inefficient and polluting, while posing significant health risks to vulnerable communities.

Existing targeted measures could reduce methane emissions from the waste sector by 29-36 megatons (Mt) per year through 2030, with the greatest potential via improved treatment and disposal of solid waste. This exceeds the total annual greenhouse gases (GHGs) emitted by electricity consumed by US households, or the emissions created by over 190 coal-fired power plants in one year.

Despite 60% of waste-sector methane abatement measures being low-cost or cost-negative, and promising various co-benefits, various financing barriers hinder their full potential.

Challenges for scaling methane abatement finance

Supply-side challenges (Funders)

- Availability of funding: There are few dedicated funding streams for methane abatement, particularly in the waste sector. Major donors and Multilateral Development Banks (MDB) tend not to prioritize methane in their climate strategies, leading to insufficient financial support.

- Fragmented funding sources: Funding for methane abatement often comes from multiple, fragmented sources, making it difficult to secure comprehensive financing for large projects. For example, a new decentralized waste management facility project may need to combine grants, loans, and private investments, each with different requirements and repayment timelines, leading to inefficiencies and delays.

- Lack of robust MRV frameworks: The absence of standardized and transparent monitoring, reporting, and evaluation (MRV) systems tailored to methane abatement is a critical challenge. Effective MRV frameworks involve systematic approaches to measuring, reporting, and verifying GHG emissions and reductions. Without these, it is challenging to demonstrate project efficacy, accurately estimate actual emission levels, attract private investment, and integrate methane-focused objectives into broader climate finance strategies.

Demand-side challenges (Project implementers)

- Project bankability: While countries have set ambitious methane reduction targets in their Nationally Determined Contributions (NDCs), translating these into viable, bankable projects at the local level remains a significant hurdle due to a lack of technical expertise and financial resources.

- High reliance on municipalities: Over 70% of solid waste management falls under municipal jurisdictions, which often lack the expertise, regulatory frameworks, and financial resources to implement methane reduction. In emerging markets and developing economies (EMDEs), waste management can represent 20% to 50% of total municipal budgets, making it challenging to allocate sufficient funds for effective waste management and related methane abatement.

- Private sector engagement: The private sector often perceives methane abatement projects as high-risk due to uncertainties in regulatory environments, market conditions, and technology performance. Such projects’ perceived low returns on investment compared to other climate investments can limit private sector engagement.

Recent progress and emerging momentum

Nevertheless, recent developments highlight growing recognition of the waste sector’s role in methane mitigation:

- Global Methane Pledge (GMP) and COP29 Commitments: At COP29, as part of the Declaration on Reducing Methane from Organic Waste, nearly USD 500 million in new grant funding for methane abatement was announced, bringing the total mobilized grant funding to over USD 2 billion. However, this remains far below the estimated USD 48 billion needed annually through 2030.

- LOW-M Initiative and regional actions: The Low-Organic Waste Methane (LOW-M) initiative aims to reduce one million tonnes of methane emissions in the solid waste subsector annually by 2030, mobilizing up to USD 10 billion in investments across 40 jurisdictions. LOW-M portfolios (target and strategic plans) created for Lagos, Nigeria, and Santo Domingo, Dominican Republic, exemplify actionable methane reduction strategies. For example, Santo Domingo aims to cut over 1,600 t/year of methane emissions by 2030 by replacing the city’s existing La Duquesa dumpsite with a new, sanitary landfill.

- Innovative regional programs: The Inter-American Development Bank’s Too Good to Waste initiative and the Recycle Organics Caribbean Program have introduced guarantees and targeted funding to accelerate methane abatement in Latin America and the Caribbean. Meanwhile, the World Bank’s Climate Change Action Plan on Methane (CH4D) channels resources to reduce methane emissions globally in the agriculture and waste sectors, with successful projects in South Asia and Sub-Saharan Africa.

While these developments are promising, faster scaling finance for methane abatement is crucial to bridge the USD 8 billion annual gap in methane abatement finance needed in the solid waste subsector through 2030 (see Figure 2). Key recommendations on how to achieve this are outlined below.

Recommendations for unlocking finance and scaling impact

- Elevate methane abatement in global climate finance frameworks: Parties to the UNFCCC can prioritize methane in climate finance goals, including methane-specific considerations in the New Collective Quantified Goal (NCQG), and establish dedicated funding streams for waste sector interventions like organic waste composting, landfill gas capture, waste diversion, and anaerobic digestion.

- Strengthen local government capacities: Multilateral donors and national governments can provide technical assistance and training to municipalities for designing and managing methane-reducing projects and expand grant and concessional financing programs for high-impact interventions.

- Mobilize blended finance instruments: Development Finance Institutions (DFI) and Multilateral Development Banks (MDB) can leverage blended finance to de-risk investments in waste-specific methane abatement projects through guarantees and concessional loans, and foster public-private partnerships for waste management solutions.

- Develop investable project pipelines: Providers of methane abatement finance can assist emerging markets and developing economies in creating investable project pipelines for waste sector initiatives, providing resources for feasibility studies and project design, and strengthen policies and regulations to ensure certainty and stability for investors.

A critical time for scaling methane abatement finance

Entering in 2025, the world has a critical five-year window to deliver on the Global Methane Pledge and reduce 30% of methane emissions[2] by 2030. Rapidly bridging methane abatement finance in the solid waste subsector through 2030 and channelling it into high-impact solutions such as organic waste management is critical. Focusing on innovative finance instruments, and community-centered solutions can also significantly contribute to broader Sustainable Development Goals (SDGs), including decent work and economic growth (SDG 8), good health and well-being (SDG 3), and sustainable cities and communities (SDG 11), creating a more sustainable, resilient, and equitable future for all.

Acknowledgments

The authors would like to thank CPI’s Baysa Naran, Ira Purnomo and Berliana Yusuf for their contributions to previous drafts of this blog/article, as well as Kirsty Taylor and Jana Stupperich for reviewing and editing.

Footnotes

[1] Full costs include hidden costs such as pollution, poor health, and climate change impacts. Net costs also account for gains from recycling minus externalities from environmental and health impacts.

[2] From 2020 levels